If you’re 12-24 months out from a potential exit, what you do during this window will directly impact your valuation, your deal structure, and whether you walk away with the outcome you actually want.

Most transportation business owners assume if they just keep growing revenue, everything else will fall into place. It doesn’t work that way.

Buyers evaluate your business through a lens you’ve probably never used: risk mitigation, operational transferability, and long-term sustainability without you.

Here’s what that means—and what you need to start doing now.

Understand the Two Categories Buyers Evaluate

When a buyer analyzes your business, they’re looking at two primary categories:

1. Valuation Drivers

These are the factors that determine how much a buyer is willing to pay. The stronger these drivers, the higher the multiple applied to your trailing 12-month EBITDA.

Primary valuation drivers include:

- Size: Revenue and EBITDA. Larger businesses command higher multiples.

- Growth trends: Year-over-year growth, especially in the current trailing 12 months.

- Gross profit margins: Higher margins signal operational efficiency and pricing power.

- Mode diversification: Businesses running multiple modes (LTL, cross-border, drayage, specialized freight) are more attractive than dry van only.

- Employee depth: Strong leadership team, documented processes, low reliance on the owner.

- Technology alignment: Systems that match the buyer’s platform or demonstrate proprietary value.

- Skillsets: Expertise in specific types of business such as LTL, Mexico/Canada cross-border, refrigeration, open-air equipment, over-dimensional, warehousing, convention, drayage, air and ocean.

2. Risk Factors

These are the factors that determine deal structure—specifically, how much cash you get at closing versus how much is tied to earnouts, and how long you’ll need to stay in the business post-sale.

Primary risk factors include:

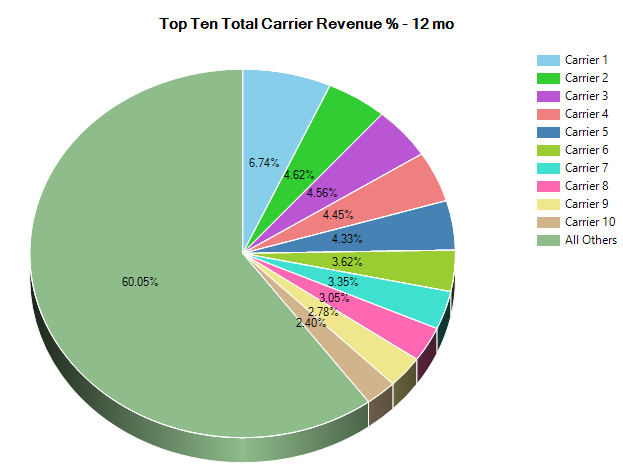

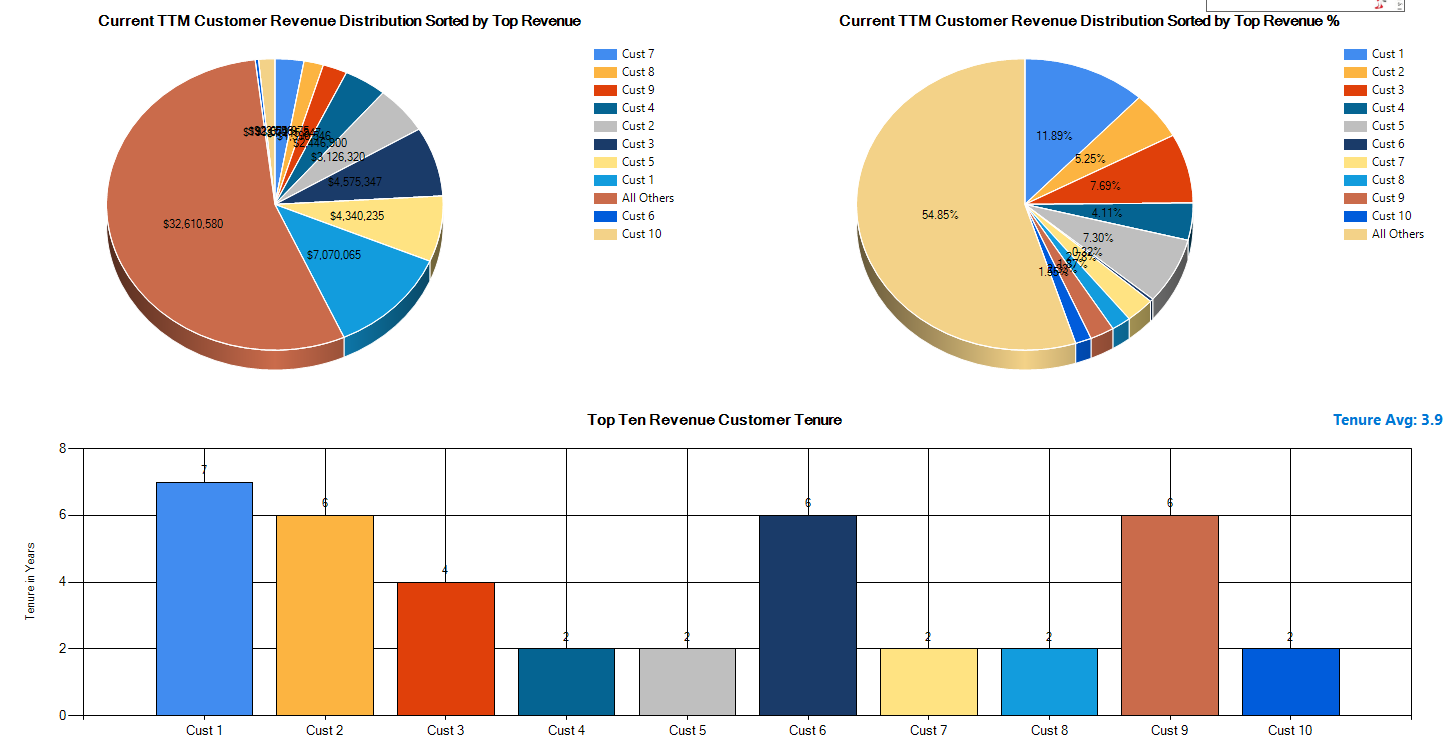

- Revenue concentration: If your top 3 customers represent 50%+ of revenue, this may impact structural terms.

- Gross profit concentration: Even more critical than revenue concentration. Losing one high-margin customer can crater profitability.

- Carrier concentration: If a high percentage of your loads move through one carrier, that’s a potential Buyer risk if that carrier is lost e

- Commodity concentration: Building materials? High risk. Food and pharmaceuticals? Lower risk.

- Sales concentration: If a high percentage of your revenue is controlled by a few people without non-compete agreements, buyers see potential transition risk.

- Customer tenure: Long-term relationships mitigate concentration risk. New customers increase it.

The higher the perceived risk the more impact a deal structure may be negatively influenced, potentially lowering the percentage of cash at close and/or lengthening the earnout period.

What to Start Doing Now (12-24 Months Out)

1. Manage Expenses Like a Buyer is Watching

Every expense decision you make in the next 12-24 months will show up in your trailing 12-month EBITDA when you go to market. That number determines your valuation.

Technology investments:

Unless your technology is truly proprietary and will drive buyer value, avoid major tech investments. Most buyers will transition you onto their platform post-close. That $200K+ TMS investment? Probably worthless unless the buyer uses the same system.

Personnel hires:

Be strategic about senior hires, especially in back-office functions. Buyers often consolidate these roles post-acquisition. Adding expensive overhead now just depresses your EBITDA.

Personal expenses:

The cleaner your books, the better. Every personal expense you run through the business becomes a “normalization” or “add-back” that buyers scrutinize. Too many add-backs can create the perception of sloppy management or hidden costs.

Wally Brauer, who built Freight Solutions from nothing in 2011 and sold it in a life-changing transaction, describes his approach:

“I was razor focused on wanting to have the strongest trailing 12 months possible. Every new hire, every purchase—if it wasn’t absolutely necessary, don’t do it. We wanted to make sure that when we got to that final goal line, the trailing 12 months was as strong as possible to drive up the highest price possible.”

2. Reduce Concentration Risk Wherever Possible

Concentration risk is the silent deal killer. You might have a $50M business with strong margins—but if your top customer represents 40% of gross profit, buyers will heavily discount your valuation or structure the deal to protect themselves.

Revenue and gross profit concentration:

Start now to diversify. Add customers. Don’t just chase revenue—chase profitable customers that reduce your concentration percentages. Buyers will look favorably on your ability to add new customers

Carrier concentration:

If you’re running a high percentage of your loads through one carrier, start building relationships with alternatives. Buyers want optionality and redundancy.

Sales concentration:

If your business lives and dies with two salespeople, you have potential risk Document processes. Cross-train. Build institutional customer relationships that aren’t person-dependent.

Buyers will analyze concentration down to granular detail—top 10 customers by revenue, top 10 by gross profit, trends over time, customer tenure as a mitigating factor. You want those charts to tell a story of diversification and stability.

3. Make Your Business Less Dependent on You

This is the hardest shift for most founders and operators to make. You’ve built this business. You know every customer, every carrier relationship, every operational nuance.

But buyers don’t want to buy you—they want to buy a business that runs without you.

Wally puts it this way:

“The fact that my company—I didn’t go into the office a lot. I had strong people that were managing the business and they all took ownership in all their different areas. If I disappear tomorrow, that business can still run on its own. And because of the ongoing relationships that the dedicated account managers had with each of these customers, I think it was deemed a lower risk.”

What this looks like practically:

- Document core processes and SOPs.

- Build a leadership team that makes key decisions without you.

- Transition customer relationships from owner-dependent to team-managed.

- Identify an “heir apparent”—someone who could run the business if you stepped away tomorrow.

The more the business depends on you personally, the riskier the deal—and the longer the earnout period maybe.

4. Understand What “Normalization” Means (And Why It Matters)

When buyers evaluate your business, they don’t just look at your reported EBITDA. They look at your normalized EBITDA—meaning they adjust for:

- One-time expenses: Large legal settlements, unusual claims expenses, non-recurring costs.

- Personal expenses: Your spouse’s salary for work they don’t actually do. Your country club membership. Your “business” vehicle.

- Anomalies: Expenses that won’t continue post-sale.

These add-backs increase your EBITDA, which increases your valuation.

But here’s the critical nuance:

The more normalizations you have, the higher the perceived risk. Buyers may start to wonder: “Are the books clean? Is this business as profitable as it looks, or is there hidden complexity?”

The cleaner your financials going into the process, the stronger your negotiating position.

5. Avoid These Common Mistakes

Waiting for the “perfect” market:

Market conditions are unpredictable. The transportation market, like the stock market, is hard to time. If you can net enough money to set a financial legacy and not have to work again, don’t gamble that guarantee for the possibility of making more.

Focusing only on valuation:

Deal structure matters as much—if not more—than enterprise valuation. A deal offering 100% cash at close will be heavily discounted. Earnout provisions, growth upsides, clawback clauses, equity retention options—these details can be worth millions. One favorable structural adjustment can offset an M&A advisor’s fee entirely.

Not understanding working capital requirements:

Most buyers require working capital to remain in the business. Working capital is defined as current assets minus current liabilities. The larger the spread between receivables and payables, the more capital is tied up in the business.

Assuming your TMS or financial system tells the whole story:

Most TMS platforms can’t generate the specific analytics buyers need: various customer metrics by specific time frames, margin calculations by mode, commodity concentration reporting, carrier dependency analysis, customer tenure trends, gross profit concentration vs. revenue concentration, origin/destination lane reporting, forms of risk mitigation reporting. Naming convention issues exist in most TMS, preventing the accurate depiction of even basic reports Buyers are interested in. The ability to consolidate reports and graphically portray data is a plus for Buyers, and will reduce the potential for error. If you can’t produce these types of reports easily now, you’ll scramble during due diligence—and buyers may question your operational sophistication.

What About Timing? When Should You Actually Sell?

This is one of the hardest questions business owners face. Here are some frameworks to consider:

Retirement Age

If you’re planning to exit at a specific age, work backward. If you want a 100% sale, plan for a 1-2 year earnout period minimum. You may need to stay in the business during that entire timeframe. Add 6-9 months for the sale process itself. If you want to retire at 62, you probably need to start the process by 60.

Market Conditions

Market timing is nearly impossible. But if you’re in a strong trailing 12-month period—revenue up, margins strong, no major customer losses—that’s your ideal window. Don’t wait for conditions to get “even better.” Markets turn fast. However, attractive deals can still be reached during soft economic times through structures that provide upside for growth.

Desire to Join a Larger Organization

Some owners sell not because they want out, but because they want in—access to stronger technology, deeper carrier relationships, enterprise-level resources. If that’s you, timing matters less than finding the right strategic partner.

Financial Legacy

Calculate your net proceeds. Account for capital gains taxes (not personal income tax rates), legal fees, accounting fees, M&A advisor fees. If the net number lets you retire comfortably and set up generational wealth, seriously consider moving forward.

A Word About Deal Structures

Most transportation deals follow one of two primary structures:

100% Sale

- Enterprise value based on normalized trailing 12-month EBITDA.

- Cash at closing: typically 60-70% (but can be lower if risk factors are high).

- Earnout period: 1-2 years (sometimes 3).

- Earnout tied to hitting EBITDA or gross profit baseline.

- Working capital stays in the business.

- Long-term debt extinguished.

- Excess cash goes to seller at closing.

Equity Retention

- Seller generally retains 10-40% equity.

- Potential higher percentage of cash at closing (because buyer carries less risk).

- Common with PE firms; some strategic buyers offer it with PUT options.

- Working capital stays in business.

- Long-term debt extinguished.

- Excess cash goes to seller at closing.

The structure you choose impacts how long it takes to fully exit and how much risk you carry post-sale.

Wally’s deal was structured with a longer earnout but without an EBITDA baseline—unusual but not unheard of:

“Mine was actually four years. They only paid me 70% upfront. The remaining 30%—10% at the end of year two, 10% year three, 10% year four. But they didn’t have an EBITDA baseline. In a normal scenario, if it falls below the baseline, that seller wouldn’t get their earnout or they’d get a discounted earnout. Mine didn’t. I feel even more fortunate that mine didn’t have a baseline.”

Every deal is different. The key is understanding what you’re trading off—cash certainty today versus upside potential tomorrow, shorter earnout versus higher valuation, 100% exit versus equity retention for a second bite.

The Bottom Line

The next 12-24 months aren’t just about running your business. They’re about positioning your business for the right buyer, the right structure, and the outcome you actually want.

Most transportation business owners wait too long, assume their financials will speak for themselves, or underestimate how much buyers care about operational transferability and risk mitigation.

The owners who get the best outcomes start preparing years before they go to market.

They manage expenses strategically. They reduce concentration risk. They build leadership depth. They make their businesses less dependent on themselves. They clean up their books. They understand the difference between valuation drivers and risk factors—and they optimize for both.

If you’re 12-24 months out from a potential exit, this is your window.

What you do now determines what’s possible later.

Ready to Start Planning?

If you’re a transportation business owner thinking seriously about an exit in the next 12-24 months—or if you’re not sure whether your business is ready—we’d welcome the opportunity to walk you through a comprehensive business analysis.

We’ll identify your valuation drivers, flag your risk factors, and give you a clear roadmap for strengthening your position before you go to market.

No obligation. No pressure. Just straight talk from people who’ve been in the trenches.

Schedule a Confidential Consultation